Memory chips arrive late in spring, but? AI ignites demand HBM "saves the field" Hynix, Samsung and other giants’ financial reports.

According to Cailian News, with the continuous injection of artificial intelligence by various capitals, the supply of high-bandwidth memory (HBM) is in short supply, and global technology giants including NVIDIA, AMD, Microsoft and Amazon are all bidding for the fifth-generation high-bandwidth memory HBM3E of SK Hynix. Recently, HBM’s "rescue" memory chip giant reported that the loss of DS department where Samsung’s electronic storage business is located narrowed in the second quarter, and SK Hynix’s sales in the second quarter exceeded analysts’ expectations. The company said that the expansion of the generative AI market has rapidly pushed up the demand for AI server memory, so the sales of high-end products such as HBM3 and DDR5 increased. Judging from the performance of the secondary market, A-share listed companies with the concept of HBM have also taken advantage of the wind. The stock prices of HBM epoxy plastic packaging supplier Huahai Chengke, HBM agent Shannon Xinchuang and HBM substrate supplier Zhongfu Circuit have increased by 157%, 158% and 136% respectively since May.

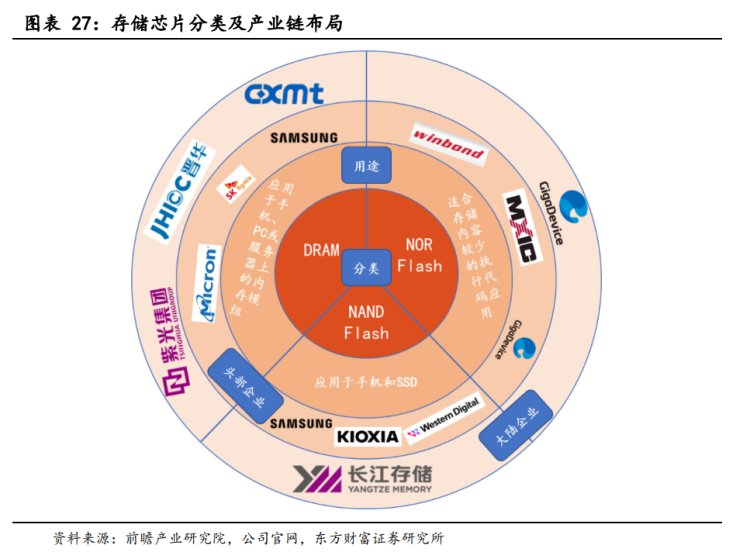

Micron Technology has previously stated that the capacity requirements for DRAM and NAND of AI servers are 8 times and 3 times that of conventional servers, respectively. Memory chips can be divided into volatile memory chips and nonvolatile memory chips according to whether data is lost after power failure. DRAM is the most common volatile memory chip, and NAND flash memory chip and NOR flash memory chip are the most common nonvolatile memory chips. According to WSTS statistics, in the memory chip market in 2021, DRAM accounts for 61%, NAND Flash accounts for 36%, and other memory chips account for only 3%.

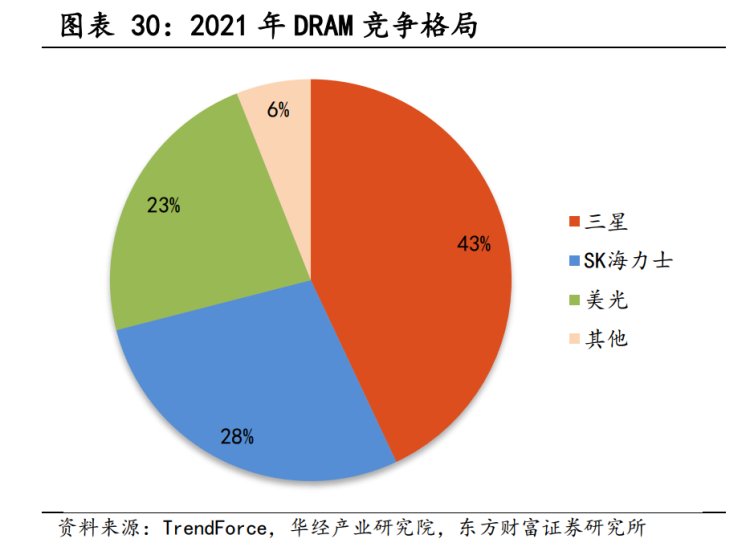

Oriental fortune securities’s February research report pointed out that DRAM’s market head enterprises are Samsung, SK Hynix, Micron, etc., and Chinese mainland’s representative enterprises include Changxin Storage and Fujian Jinhua. The market head enterprises of NAND Flash are Samsung, Chivalrous, Western Digital, etc., and the representative enterprises of Chinese mainland are mainly Changjiang Storage; NOR Flash’s market head enterprises are Winbond, Wanghong, Zhaoyi Innovation, etc., and Chinese mainland’s representative enterprises are mainly Zhaoyi Innovation.

▌ SK Hynix, Samsung and Micron, the three leading global memory chips, pointed out that the price, supply and demand and space end blew the horn of industry recovery.

HBM is a DRAM product with the fastest data processing speed. It is a DRAM memory chip based on 3D stacking technology. After stacking multiple DDR chips, it is packaged with GPU, which can achieve higher bandwidth, higher bit width, lower power consumption and smaller size. The latest financial report shows that the performance of SK Hynix, Samsung and Micron, the three leading memory chip DRAM, began to rebound. Samsung Electronics 23Q2′ s revenue declined due to the decline in smartphone shipments, but its storage business improved compared with the previous quarter. The official said that it was mainly due to the company’s focus on HBM and DDR5 products; SK Hynix’s sales in the quarter ended June 30 were 7.31 trillion won (about 5.7 billion US dollars), down 47% year-on-year, but exceeding analysts’ expectations of 6.05 trillion won. Although HBM’s revenue in SK Hynix currently accounts for less than 1%, this proportion is expected to rise to 10% this year; Meguiar’s 23Q2 performance rebounded after three consecutive quarters of decline. In addition, the monthly performance of the original factory in Taiwan, China also improved continuously month on month.

The research report released by Pan Chang, TF Securities on July 17th pointed out that recently, the favorable turning point of memory chips has been frequently reported, and the horn of recovery seems to be in our ears. From the perspective of historical cycle, the cycle of the storage industry is about 3-4 years. This cycle starts from 2020Q1, and the price peaks in stages in 2022Q1. At present, the price has been reduced for six consecutive quarters, and it is in the bottoming stage of the cycle.

In terms of price, since Q2 this year, a number of suppliers have issued bottoming signals. First, Samsung and Micron issued a notice to dealers, no longer taking orders from DRAM and NANDFlash at low prices, and refused to accept quotations lower than those in April. In May, it was reported that Samsung Electronics and SK Hynix were considering raising their quotations after the original flash memory of Changjiang Storage officially started to increase its price by 3-5%. In late June, only Samsung was willing to conduct cSSD (Consumer Solid-State Disk) transactions in advance, and the dealers hoped that the suppliers would make concessions, but they were all rejected.

Pan Wei pointed out that on the demand side of supply, Micron announced in June that it expected to reduce production to 2024. Earlier, in 2022Q4, the original factories drastically cut their capital expenditures. If the normal production cycle is 3-4 months, the effect of supply contraction and production reduction will be accelerated in Q2 and Q3. South Asia Branch said that the company had urgent orders in some application fields. Recently, Winbond’s demand for three major applications, such as consumer electronics, television and Internet of Things, has warmed up, and industrial control-related orders have continued to be hot, and customers have rushed in, and there are also a lot of them.

In addition, on the space side, in the short term, the scale of memory chips will increase quarter by quarter, and in the long term, the storage demand under the catalysis of AI is expected to increase several times. On the geopolitical side, overseas manufacturers gradually withdrew from the niche market, and Meguiar’s incident accelerated local substitution.

▌ The memory chip will be reversed or "late" at the bottom. In the two quarters, the organization expects DRAM or NAND Flash to recover the cross-border layout of many A-share listed companies faster.

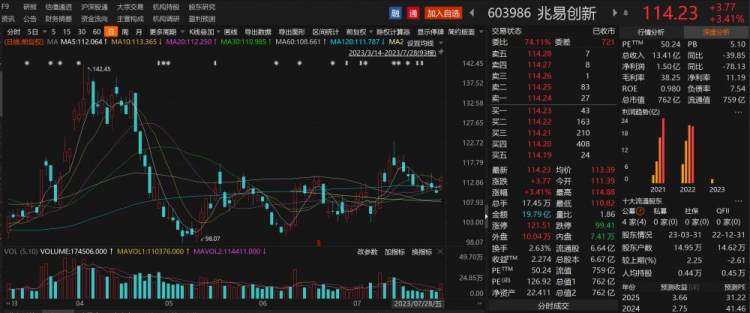

It is worth noting that at present, the memory chip industry seems to be confirming that it is about to bottom out, but the share price of 76 billion A-share leader Zhaoyi Innovation is "still calm". In fact, the impending reversal has even been "late". Recently, Yole Intelligence, a market research organization, updated a monitoring data report of the memory chip market. In Yole’s original forecast, the global memory chip market will start to recover in the second quarter of 2023, but its latest report points out that there is no need to hold too much hope for the memory chip market in the third quarter of 2023, and it is optimistic that the market will start to pick up in the fourth quarter of this year.

However, Yole is not the only one who predicts that the storage market will recover in the coming fourth quarter. According to Taiwan Province Economic Daily and Science and Technology News, citing the latest report issued by the American market research organization, Micron, Western Digital and other memory chip suppliers think that the product prices have fallen to the bottom, and began to cancel the mode of bulk trading at discounted prices in advance, and even began to raise prices. The survey agency predicts that the decline rate of memory chip prices will narrow from Q3, and the contract prices of some products are likely to rise from Q4. The situation of different product lines is different, and it is expected to fully recover next year.

Judging from the market news, the recovery of DRAM may be faster than that of NAND Flash. TrendForce Jibang Consulting recently estimated that the average price of NAND Flash in the third quarter continued to drop by about 3%-8%, and it is expected to stop falling and rebound in the fourth quarter, and the average price decline of DRAM in the third quarter will converge to 0-5%. The article "The Cold Wind of Memory Chips, Will Stop" published by the semiconductor industry on July 25th pointed out that DRAM bottomed out in the third quarter and NAND waited for another season. Earlier, some people in the industrial chain said that Samsung, SK Hynix and Micron all hoped to raise the contract price of DRAM orders in the third quarter, with a target increase of 7%-8%. However, because the terminal market has not seen obvious signs of recovery, there are obvious signs of seesaw in the upstream and downstream. In terms of NAND, recently, the market also heard that the original upstream NAND factory plans to raise the price from July.

In addition, according to the information of the Internet Office in May, Micron, which occupies a lot of land in China storage market, failed to pass the network security review. Ping An Securities Research Report pointed out that in 2022, Micron’s operating income in Chinese mainland was $3.311 billion. Analysts pointed out that if Micron’s business in China is limited, the niche storage market will naturally benefit first. In the niche storage field with relatively low technical barriers, Zhaoyi Innovation is the fastest growing and strongest company. In addition, Beijing Junzheng, the leader in vehicle storage, and Dongxin, the leader in domestic SLC NAND field, are expected to benefit. In the downstream storage module industry, Jumbo Long and Baiwei Storage also have strong competitiveness in the global market, among which Jumbo Long’s eMMC and UFS products have a global market share of 6.5%, ranking sixth in the world and first in China; The global market share of eMMC and UFS stored by Baiwei is 2.4%, ranking eighth in the world and second in China. The main suppliers of these two companies include Micron.

Analysts pointed out that although the inventory pressure downstream of memory chips is still there, the bottom is just around the corner through the dynamics of major manufacturers and industry analysis data. In order to catch up with the next wave of boom cycle after the turning point of the industry, Wanrun Technology, Liyuan Information, Shannon Core and Guoxin Technology and many other manufacturers have cross-border layouts. However, analysts also pointed out that even if the existing domestic storage companies, such as Zhaoyi Innovation, Beijing Junzheng, Eastcore and Puyan, are counted, most of the domestic storage products are at the SSD module and NOR Flash level, and it is difficult to touch the high-end DRAM and other markets vigorously promoted by international manufacturers, which makes it difficult for domestic storage manufacturers to enjoy the dividend in the incremental market and need to follow the trend in the supply and demand of the storage market.

Original title: Memory chips arrive late in spring? AI ignites demand for HBM to "rescue" the financial reports of giants such as Hynix and Samsung. Can A shares fully blow the "counterattack assembly number"

Editor: Lareina C

Editor: Wu Zhonglan

Audit: Feng Fei